��һ����������

| ��վ��ҳ | ���ڽ��� | ���� | ��Ʊ | ���� | ���� | �ڻ� | ���� | �۹� | ���� | ��� | ծȯ | �ƽ� | ���� | ���� | ���� | ���� | �������� |

|

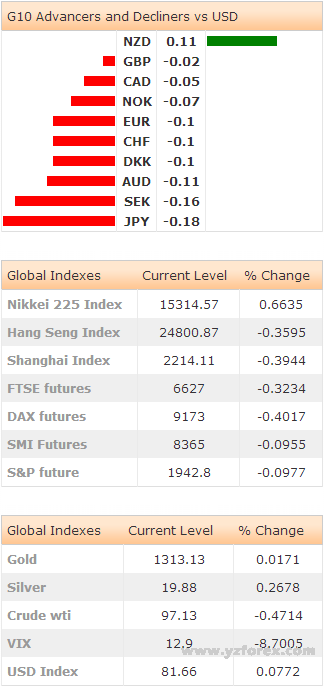

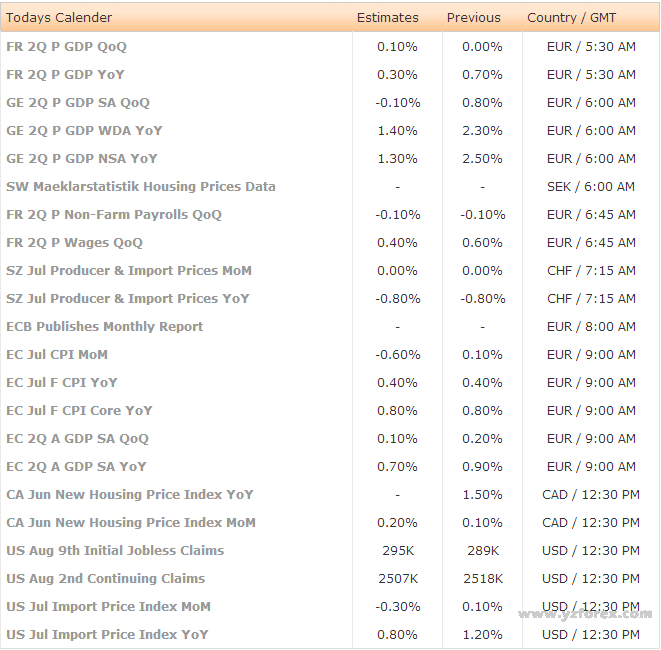

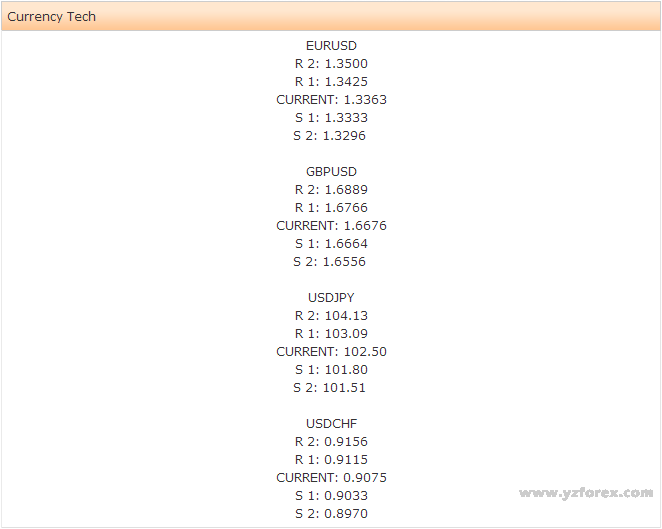

���ڵ�Ե���ν��ž��Ƴ��ֻ��⣬��������߹�ע����ת���¼�/����֮�ϡ��Զ����г����̣���Ԫ����Ԫ¼����������ԭ�����GDP���������ش��������ڶ����ȳ�ֵ�����껯���µ�6.8%��֮�⣬6�»�е����������������Ҳ�����е���Ҫ������ʵ��ֵΪ8.8%��Ԥ��Ϊ15.3%��ǰֵΪ�µ�19.5%����4-6�¼���������10.4%����Ԥ��7-9�½�Ϊ�ֹۣ�·������Ϊ��������2.9%���������г������ձ����л�ʵʩ����̼���ʩ����Ԫ������Ӯ�������þ��ۡ���Ԫ����Ԫ��ס��200���ƶ����ߣ�ǰ����λ��֧��λ������������102.66����ֹд����ʱ��������������λ��103.00ǰ����������˴�ˮƽ��Ӧ���������ͷ��ͷ��ŷԪ����Ԫ������·�϶�21���ƶ����߽����˲��ԣ���ŷԪ�Ծ���������ѹ�������� ��ŷԪ����7��ͨ��������ֵ�Լ��ڶ�����GDP��ֵ���ڽ����ͷš�Ԥ�����������������ƫ��Ϊ�ᶨ������������������1.3415�����˿��ٻ������¡�������1.3296-1.3333��2013��11����ͼ�-8��6����ͼۣ��������ȶ�֧�š��������̼۸���1.3345��MACD����㣩��Ӧ���ܹ�ά��ƣ����ŷԪ���С������۷ֲ���1.3400-25����Ȩ�Է���-21���ƶ����ߣ��Ϸ������DZ��ַ��������ƫ����ŷԪ��Ӣ����0.80000�Ϸ����н��ף���������֮ǰ����Ȩ�ϰ��ȶ���0.80500-0.81000������ ��Ӣ����ƽ��������������������������ʧҵ�ʺ͵Ǽ�ʧҵ�ʽ�һ�����ƵĻ����ԡ�Ӣ������Ԫ����ת���ºͣ�ԭ����5�¼���ͨ�����ͱ��潫��ȹ�������Ԥ���2.50%�µ���1.25%��Ӣ�������г������ʾ�����ھ��ö�ƫ�����������ʻ�����η�Ӧ�в�ȷ����������ؼ���ʵʩ�״μ�Ϣ�ж���Ӣ������Ԫ������1.6670���ؼ�֧��λλ��200���ƶ����ߣ�1.6664��������״�������ǿ��ָ����26%��30�ղ��ִ���Ե��1.6683���������ڵ�ǰˮƽ����ͣ�١����� �������ڶ������������ۣ��ų�ͨ���������أ�����1.2%��ǰֵΪ0.7%������ʹŦԪ����Ԫ�������г�Ӯ������Ƿ����û��ҶԷ�����0.8489����0.8500ǰ���������������˷��������ڿ�����ͷ����������ͻ��0.8500-25����������λˮƽ-MACD����㣩��Ӧ�û�������ڿ�����ת�����쵽�ڵ���Ȩ����λ��0.8425-45�����ϰ��趨��0.8550��ŦԪ����Ԫͻ����200���ƶ����ߣ�86.622�������ڷ���ƫ�ñ����ȶ��������������һ��������������һĿ������Ƹǣ�87.786-88.580����չ����Ԫ��ŦԪ������dz���ƽ����Ԫ��ŦԪ�Ľ������Ծ�ճ��1.0911-1.1040��38.2%��쳲�����ˮƽ-2013��11����2014��1���µ�ʱ50.0%��쳲�����ˮƽ���������ڽ��н��ס�Ϊ�����µĶ��ڷ�չ��������ƴ����������һ�ߡ����� ŷ�����н��ڽ����ͷ��¶ȱ��档ֵ�ý����߹�ע�Ļ��У��������¹���ŷԪ���ڶ�����GDP���Ⱥ���ȳ�ֵ�������ڶ����ȷ�ũ��ҵ���ʳ�ֵ����ʿ7�������ߺͽ��ڼ۸����ʺ����ʣ�ŷԪ��7��CPI���ʺ�������ֵ�����ô�6���·��۸�ָ�����ʺ����ʣ�����8��9���״�ʧҵ�ȼ�����������8��2�ճ���ʧҵ�ȼ����������Լ�����7�½��ڼ۸�ָ�����ʺ����ʵȡ����� The FX traders��focus shift to economic events/data as the geopolitical tensions de-escalate.The Japanese Yen recorded the largest downside versus USD since Tokyo open as,on top of the significant contraction in GDP(-6.8%q/q annualized according to 2Q(P)data),the machine orders grew at slower pace of 8.8%in month to June(vs.15.3%exp.&-19.5%last).The April-June contraction has been-10.4%on quarter,although the expectations for July-September are more optimistic(+2.9%q/q on Reuters poll).JPY crosses were well bid on speculations for more BoJ stimulus.USD/JPY hold support at the 200-dma(former resistance)and advanced to 102.66(at the time of writing).Offers line up pre-103.00,if cleared,should boost the bullish momentum.EUR/JPY tests the 21-dma on the upside.EUR remains under selling pressures.���� Euro-zone July final inflation and 2Q preliminary GDP data are due today.Expectations are soft,the bias is firmly negative.Yesterday��s spike to 1.3415 triggered rapid profit taking.We see solid support zone at 1.3296/1.3333(Nov 2013 low/Aug 6th low).A daily close above 1.3345(MACD pivot)should keep the EUR bears timid.Offers line up above 1.3400/25(optionality/21-dma).We remain seller on rallies.EUR/GBP trades above 0.80000,option barriers are solid at 0.80500/0.81000 before the weekly closing bell.���� In the UK,the contraction in average wage growth offset enthusiasm on further improvement in unemployment and claimant count rate.The sentiment in GBP/USD turned mild as the quarterly Inflation Report revised the annual wage growth forecasts down to 1.25%from 2.50%in May.The BoE Governor Carney said there is no rush for the first rate hike given the uncertainties on how the economy would react to tighter bank rates.GBP/USD sold-off to 1.6670.The critical support stands at the 200-dma(1.6664).The oversold conditions(RSI at 26%,30-day lower BB at 1.6683)suggests a pause at the current levels.���� Kiwi gained the most vs.USD in Asia as the NZ retail sales(ex-inflation)advanced 1.2%in the second quarter(vs.0.7%a quarter ago).The pair rallied to 0.8489,offers pre-0.8500 capped the rally.As the bearish momentum slows,a break above 0.8500/25 region(psychological level/MACD pivot)should suggest a short-term bullish reversal.Option bids are placed at 0.8425/45 for today expiry,the first set of barriers appear at 0.8550.NZD/JPY sits above its 200-dma(86.622).Technicals suggest further gains towards the daily Ichimoku cloud cover(87.786/88.580)as risk appetite stabilizes.AUD/NZD technicals are perfectly flat,the antipodean cross remains stuck within 1.0911/1.1040 range(Fib 38.2%&50.0%levels on Nov��13�CJan��14 drop).Breakout on either side is required to define fresh short-term direction.���� The ECB publishes monthly report today.Traders watch French,German and Euro-Zone 2Q(Preliminary)GDP q/q&y/y,French 2Q(P)Nonfarm Payrolls and Wages,Swiss July Producer&Import Prices m/m&y/y,Euro-Zone July(Final)CPI m/m&y/y,Canadian June New Housing Price Index m/m&y/y,US Aug 9th Initial Jobless Claims&Aug 2nd Continuing Claims and US July Import Price Index m/m&y/y.���� |

|

||

|

|

||

| ÿ�ձض� | |

|

�� �Ĵ�ͷ��

�� ÿ�ս�����ʾ �� ÿ�����й��� �� ÿ�ջ��й��� �� ÿ�������� �� ÿ��Ҫ�ŵ��� �� ÿ���г����� �� Ȩ֤������Ϣ �� ������������ �� �������ռ��� �� �������ռ��� �� һ�ܽ��ױ���

�� ����������Ϣ �� ����������Ϣ �� ���ǵ������� �� ���ǵ������� �� ����ͣ��һ�� �� ����ͣ��һ�� �� ��С����Ϣ�� �� �ڻ�ÿ����ʾ �� ������������ �� ������������ �� �ƾ�����

�� ����ÿ�վ�ֵ �� ÿ���ֻ��۸� �� ÿ���������� �� �Ϻ��ƽ����� �� �ؽ������� �� ����ԭ���г� �� �����ڽ����� �� ŦԼ�ڽ����� �� ծȯ����������ʾ �� ���ǻ����� |

|